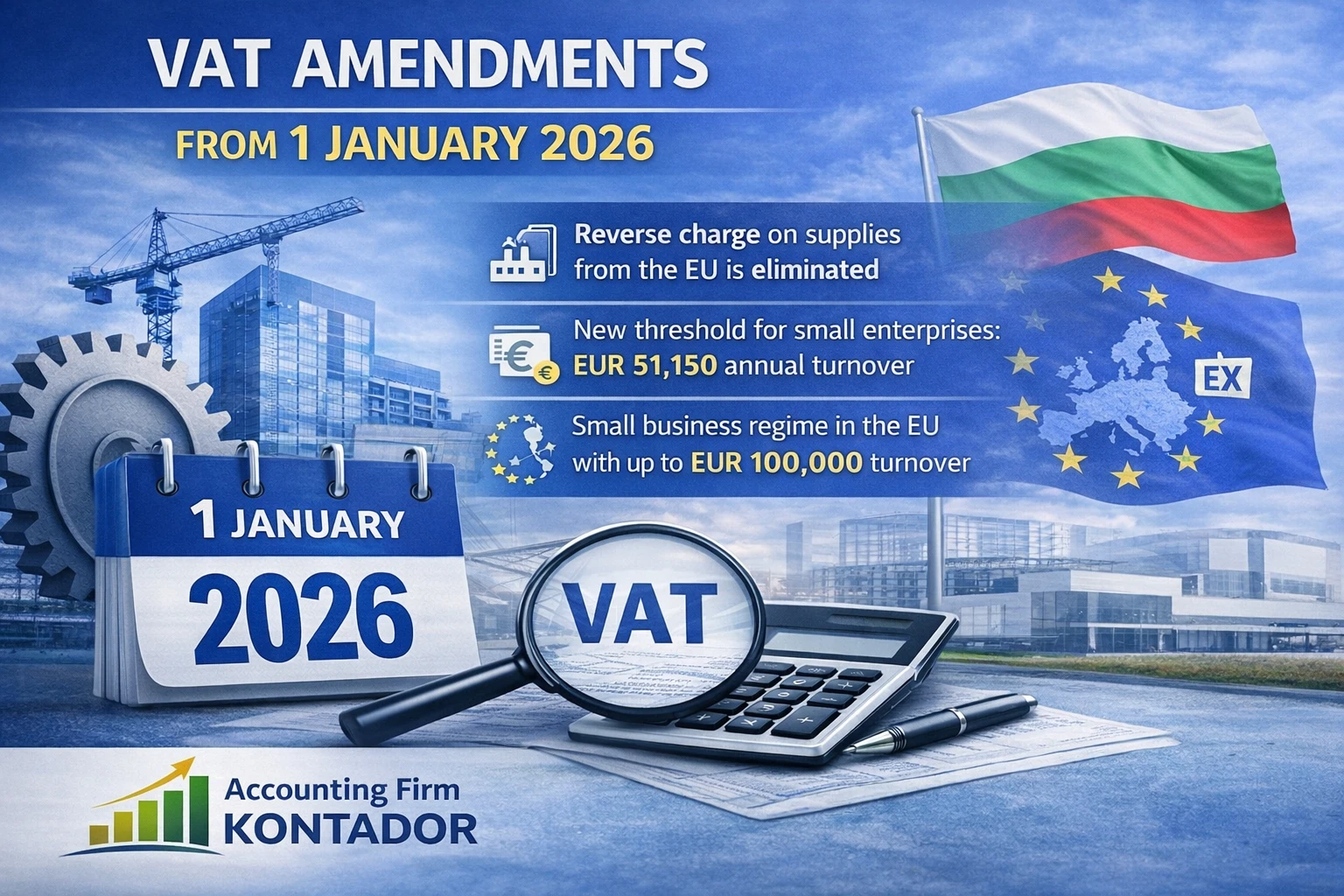

Еffective 1 January 2026

Discontinuation of the reverse charge mechanism for supplies of goods accompanied by assembly/installation

As of the beginning of 2026, the VAT treatment of supplies of goods where the assembly or installation on the territory of Bulgaria is performed by the supplier or at their expense is amended.

For suppliers established in an EU Member State, the reverse charge mechanism will no longer apply.

Instead, where such EU-based suppliers carry out supplies of goods with assembly/installation in Bulgaria, they will be required to register for VAT in Bulgaria before performing their first taxable supply.

For suppliers established outside the EU, the rules remain unchanged — the obligation to register for Bulgarian VAT continues to apply.

The amendment requires businesses to review existing contractual arrangements with foreign suppliers to ensure correct VAT treatment after 1 January 2026.

Introduction of new regimes for small enterprises

The amendments to the VAT Act transpose the EU rules regarding VAT simplifications for small enterprises and introduce two regimes:

Small enterprises regime applicable in Bulgaria

The existing exemption from VAT registration is retained, with several key modifications:

- The registration threshold is set at EUR 51,130 per calendar year, rather than on a rolling basis.

- When calculating turnover, certain exempt supplies are now included, including transactions related to real estate.

- Persons who exceed the new threshold during 2025 must submit a VAT registration application by 8 January 2026.

EU small enterprises regime

A new option is introduced allowing small enterprises established in one EU Member State to benefit from VAT exemption on supplies carried out in other Member States under specific conditions:

- Registration is made by submitting an application specifying the Member States in which the exemption will apply.

- Businesses operating under this regime are not entitled to input VAT deduction on goods and services acquired for making such exempt supplies.

- A new form of VAT identification is introduced, whereby the VAT number will end with the suffix “EX”.

- To qualify, the total annual turnover within the EU must not exceed EUR 100,000.

Additional amendments

The law also introduces corresponding revisions and technical adjustments to other provisions of the VAT Act in order to align national legislation with the new rules.

For more questions, the team of Accounting Firm KONTADOR is available to provide professional consultation.