INCOME TYPE CODES UNDER ARTICLE 73 OF THE BULGARIAN PERSONAL INCOME TAX ACT – A PRACTICAL GUIDE

The income type code nomenclature is a key element in the correct reporting of individuals’ income to the Bulgarian National Revenue Agency. These codes are used when preparing the annual statement under Article 73 of the Personal Income Tax Act (PITA), as well as for annual personal income tax returns, and they directly affect the applicable tax treatment.

Selecting an incorrect income code is not a minor technical issue. It may lead to inconsistencies between submitted data, requests for corrections, inquiries from the tax authorities, and potential penalties. Therefore, the correct application of income type codes is essential.

- Income Subject to Taxation on the Annual Tax Base

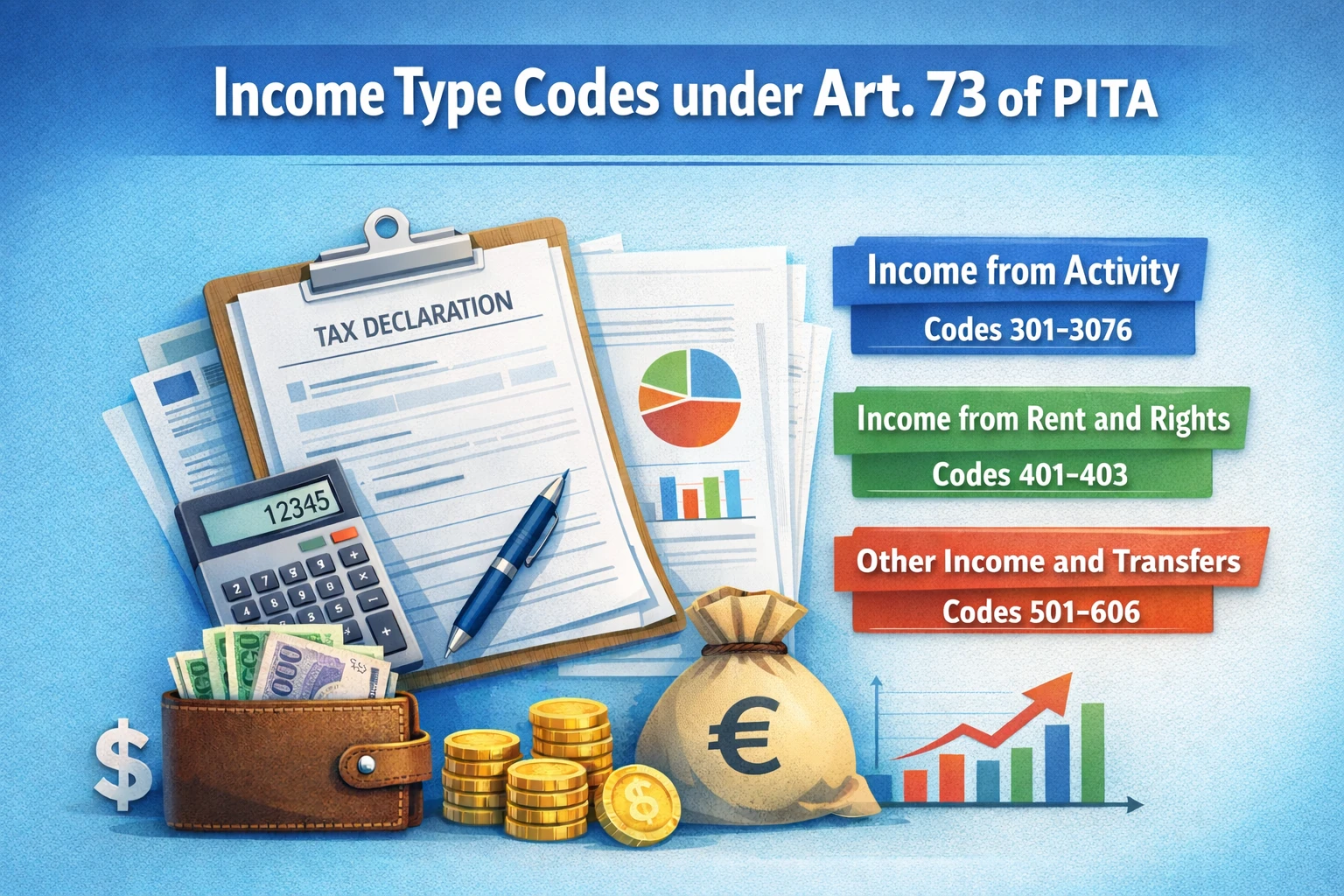

Income from Economic Activity and Non-Employment Relationships (Codes 301 – 30714)

This category includes the most common types of income earned by individuals outside employment relationships.

Code 301 applies to income from activities as a registered agricultural producer for the production of unprocessed agricultural products, excluding decorative plants.

Codes 302 and 303 cover income from processed or unprocessed agricultural products, as well as income from forestry, hunting, and fisheries.

Code 304 is used for copyright and licensing remuneration, including income from the sale of scientific, cultural, or artistic works by their authors.

Code 305 applies to income from craft activities not subject to patent tax.

Code 306 is used for income earned from exercising a liberal profession.

Of particular practical importance are codes 3071 – 30714, which apply to income from non-employment relationships, categorized by type of service. These include financial and insurance intermediation, consultancy services, accounting and legal services, IT services, transport, construction, repairs, education, healthcare, and other services.

For example:

- consultancy services under a civil contract are reported using code 3073;

- accounting and legal services are reported using code 3074;

- when the activity does not clearly fall into a specific category, code 30714 – other non-employment relationships is used.

- Income from Rent and Granting of Rights (Codes 401 – 403)

Code 401 is used for income from renting out immovable property where no transfer of ownership is provided.

Code 402 applies to income from renting movable property.

Code 403 is used for remuneration under franchise, factoring, and other agreements for granting rights for use.

III. Income from Other Sources under Article 35 of the PITA (Codes 601 – 606)

This group includes:

- compensation for lost profits and penalties;

- cash and non-cash prizes from games and competitions;

- interest income;

- dividends from cooperatives;

- income from exercising inherited intellectual property rights;

- other income not classified under previous categories.

- Income from the Transfer of Rights or Property (Codes 501 – 509)

This section includes income from the sale or exchange of immovable and movable property, financial assets, shares, equity interests, foreign currency transactions, and leasing arrangements with explicit transfer of ownership.

A common mistake is confusing taxable income from the sale of property with income that is exempt from taxation, which makes careful classification particularly important.

- Income Subject to Final Withholding Tax under Chapter Six of the PITA (Codes 801 – 821)

These types of income are subject to final withholding tax and are not included in the individual’s annual tax base.

They include:

- rental income;

- dividends and liquidation proceeds;

- interest income;

- copyright and licensing fees;

- remuneration for management and control;

- income from the sale of immovable property where final taxation applies.

- Non-Taxable Income Reportable When Exceeding BGN 5,000 Annually (Codes 901 – 907)

Under Article 73, paragraph 1, item 4 of the PITA, certain non-taxable income must still be reported if its annual amount exceeds BGN 5,000. Such income includes:

- income from financial instruments;

- income from supplementary voluntary pension schemes;

- interest from government and municipal bonds;

- winnings from licensed gambling activities;

- income from rent or lease of agricultural land.

Common Mistakes in Applying Income Type Codes

The most frequent errors include:

- selecting a code based on assumption rather than the actual nature of the income;

- confusing liberal professions with non-employment relationships;

- using an incorrect code for rental income;

- discrepancies between the Article 73 statement and the annual tax return.

Conclusion

Income type codes are not a formality but a fundamental element of proper tax reporting. Choosing the correct code ensures accurate reporting to the tax authorities, prevents unnecessary corrections, and avoids administrative complications. When there is uncertainty regarding the applicable code, consulting a professional accountant is strongly recommended to ensure lawful and accurate income reporting.